Deprecated: Creation of dynamic property OMAPI_Elementor_Widget::$base is deprecated in /home2/inancjw3/public_html/wp-content/plugins/optinmonster/OMAPI/Elementor/Widget.php on line 41

When you think budget you probably think limited, right?

When you think budget you probably think limited, right?

Most people approach the idea of having a budget as limiting themselves on what they can and cannot spend money on.

Used correctly though, that could not be farther from the truth!

A budget brings financial success.

A budget is a spending plan that empowers you to take ownership of your finances to maximize the usage of your income so you can achieve your goals stress free and without going into debt.

What is a Budget?

A budget is simple – it tells you how much you have to spend and then allows you to keep track of what you spend so at the end of the month you spend less than you made.

That’s it.

A budget doesn’t take money away from you. Rather, a budget simply gives you the data you need to manage your money.

When I work with my clients, I like to refer to them building a spending plan rather than a budget.

Everyone has plans. We have plans through the work day on how we will allocate our time to get our duties efficiently done. We have a plan what we will eat for dinner and how we will manage the time of all our kids after-school commitments.

You already budget! The idea of budgeting isn’t a foreign one to you. Your whole life is budgeting to maximize your goals and time.

Every time you make a grocery list, you are budgeting! You don’t want to buy something if you aren’t going to use it. But in order to know what to buy, you first have to plan.

The same goes with your finances.

How are you to maximize the money you have worked so hard for, if you don’t know how much you have and what you are spending it on? The answer is simple. You can’t. You need a budget.

How do you create a budget?

A budget, or spending plan, is a simple four step process.

Step One

Step One

See how much post-tax income you bring home each month.

This should be done as an average of at least 2 or 3 months and here is why.

Some people’s income changed through the year based on overtime, having summers off as a teacher, lower commission sales and many other reasons. If you for instance base your year’s total on the month you had the best sales of your career, then the number you come to will be disproportional and inaccurate giving you’re an incorrect base number to work off of.

I would MUCH rather you work off a lower number than what you actually make and have extra money at the end of the month than have your base budget be more than what you actually make.

As you do this for more months, I also encourage you to redo this as you may have missed some income or your income may have changed.

Another important point is that this is post tax income.

Rather than doing pre-tax income and then having to do calculations to see how much you actually have once you have paid the government, just make it easier on yourself and take what you are actually able to spend on yourself post tax.

Step Two

Track your expenses to see how much you spend each month.

Once again, this should be done as an average of at least 2 or 3 months for similar reasons.

You do not spend the same each month. I guarantee. My wife and I have a budget that we follow and I have a dollar amount for my electric and gas bills in my budget.

The problem with both categories is that they can literally fluctuate by upwards of 40-50% month to month depending on the season. That example is just a small example when it comes to everchanging expenses.

We all know car and house repair’s always come up. What you spend in December is always different than what you spend in July because of Christmas.

For steps one and two, I do not want you to stress out about finding the exact dollar amount for the rest of your life.

The budget will change as you and your money habits change. If you get a promotion, you can increase your income and thus your budget. If you lose a job, the opposite will happen. When you have a child, expenses raise!

A budget is always changing, so just do your best for this first budget.

Step Three

Figure out what budget plan you want to use.

When I say budget plan, I mean the system you are going to use to categorize your spending. While there are many different kinds and twists on budgeting plans, I recommend using one of two plans.

Proportional budget

With the proportional budget plan, essentially what you do is break your income (which starts at 100%) into broad subcategories that each get a certain percentage.

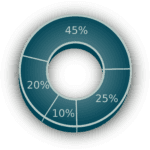

The most common is the 50/30/20 budget.

In this specific budget plan, you break out 50% of your total take home to needs, then 30% to wants, and the remaining 20% to savings.

These numbers can obviously be changed a bit.

Let’s say you want to save 25% of your income. In that case, you would change savings to 25% and maybe switch wants to 25% making the new budget a 50/25/25.

The main issue with this budget is the difficultly we all have of separating needs and wants.

Essentially, what we are doing is trying to categorize our values into two broad categories while at the same time trying to rationalize what’s important to us verses what is actually important.

So for example, which category would you put eating out into? Is that a need, or is that a want?

For my wife and I, we go out at least once a month on a date night. While that may seem like a plushy want to some people, it is a need for us because of the quality time and conversation is allows us to have each month.

This is not a bad plan though.

For many people this is the best plan for three reasons.

One, it does not require a ton of time in specific itemizing of every expense.

Two, some people are just better at finding what is really important to them and delegating the nonessentials to the wants category.

And three, this plan puts a major emphasis on saving which is vitally important.

Zero-Sum budget

This spending plan is much more detailed and thorough. This plan will take more work. However, this is the plan that I personally use and I find it works best for me.

A zero-sum budget is where you classify all your expenses into specific categories and then allocate each category with a certain amount of money to be used each month. Each category, once added up, should equal the total amount of income you have for the month with zero dollars remaining.

A zero-sum budget is where you classify all your expenses into specific categories and then allocate each category with a certain amount of money to be used each month. Each category, once added up, should equal the total amount of income you have for the month with zero dollars remaining.

The reason I like this plan is because there limited emotional interaction.

Much like the previous budget, I know the categories I need to spend on such as housing, food, transportation, saving and giving. I can then add categories that may be more wants: house furnishings, vacation, eating out, clothing upgrades, etc.

When finished, I have all my categories written out, and then I go through my expenses and put a dollar amount to each category until I have equaled the total amount I have for the month.

When an expense comes up, I don’t have to guess whether I need it or want it. With a zero-sum budget, I either have the money for that or I don’t.

The main con with this is the amount of time it takes to complete at first.

When I first did it, I needed to specifically itemize each of my expenses and put everything into categories. Now that I have done it for a while, and have my basic budget set though, it can easily be upgraded as my budget changes.

Step Four

Follow through.

Step four is probably the hardest step of them all. This step is where the rubber meets the road and you really have to decide how important financial ownership is to you.

There are a few ways to help make it easier:

- Envelopes – take out cash each month you will use for certain categories you have trouble sticking with. If eating out is an issue, take out $100 dollars and once that cash is gone, you can’t eat out anymore.

- Accountability – have a friend keep you accountable. Even better, have your spouse keep you accountable! Be open and honest with your finances. There is nothing to be ashamed of. You spend money. So does everyone.

- Find a budgeting tool that works for you. This is addressed next in more detail.

What tools are there to help me?

What tools are there to help me?

There are a multitude of different budgeting apps and documents you can use to help you create and track your spending. If used correctly, these can drastically simplify your budgeting process. Below I want to briefly look at a few of them.

- YNAB – You Need A Budget, or YNAB, is a popular but pretty expansive program. It is zero-sum based and does have an annual cost of $99 which, at an up front cost saves from the $14.99 a month charge. With it you can set goals, get tangible reports and sync to your bank for easier connection and downloads of expenses.

- EveryDollar – This is similar to YNAB in that it is a zero-sum based app as well. This app is a feature from Dave Ramsey so if you are familiar with his teachings, this may be the way to go. They have both a free version and a paid version which provides more perks.

- Excel – This is actually one of the ways that I budget. What I’ve done is make my own Excel document and I export my expenses each month from my bank via a CSV file and then break down my budget accordingly. It takes more work but is essentially the same thing as YNAB and Every Dollar but is free.

- Mint – Mint is from Intuit and is free. It offers a free platform to begin budgeting with many of the pros of the above apps but only allows you to budget one month at a time which some find limiting.

Should I have a budget?

The answer is a resounding YES! Yes, you should have a budget!

If you want to stop living paycheck-to-paycheck, start focusing on saving, and really achieve your financial goals then a budget is a must have for you.

A budget provides knowledge. Once you truly understand what you are spending on and how much you are spending, you can finally take control of your finances rather than your finances controlling you.